For business owners and HR professionals, the road ahead for California’s 2026 small group medical rates is looking bumpy. With premium rates on the rise and the future of federal subsidies hanging in question, your company’s healthcare budget is facing a perfect storm of uncertainty.

This year’s shifts go far beyond the typical annual rate adjustments. Small business leaders must proactively prepare for the dual threat of underlying healthcare inflation and the potential expiration of enhanced premium tax credits. If the premium tax credits are not extended in the individual market, it will cause a trickle-down to affect the group market where premiums will be impacted.

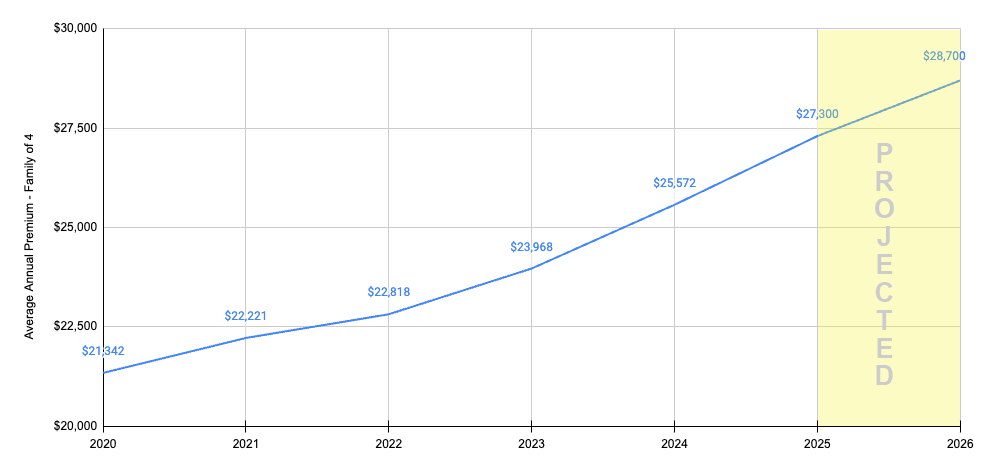

California small business health insurance premiums are projected to rise dramatically, with initial reports suggesting an average rate increase of 10.3% for 2026. The actual rate increases will vary by insurer, but factors like general inflation, the rising costs to deliver healthcare and higher pharmacy utilization, are contributing to the premium hikes. For many, this means a dramatic spike in monthly costs, impacting both your company’s bottom line and your employees’ wallets.

Possible Health Insurance Premium Rate Hikes and Subsidy Cuts

The Rate Surge: A Closer Look

Industry analysts and state officials have confirmed that escalating medical and pharmaceutical costs are driving significant increases in 2026 premiums.

- Average Increases: Initial figures from sources like Covered California indicate substantial average rate increases across the board. Specific examples from Covered California for Small Business show proposed hikes ranging from +7.1% to over +20% depending on the carrier.

- Pharmacy Utilization: increasing utilization of high-cost specialty drugs, particularly the expensive GLP-1 medications for obesity and other conditions, and the broader emergence of new, expensive treatments like gene therapies and biologics.

- Risk Pool Concerns: Some carriers are pointing to “worsening risk pools” within the small group market as another reason for these higher rates.

It’s crucial to look beyond the average. The wide range of increases means that your company’s specific plan could be hit much harder than the overall market trend.

California’s 2026 Small Group Medical Rate Trend

The Subsidy Cliff: A Looming Financial Shock

The enhanced federal premium tax credits, which have been a financial lifeline for millions, are scheduled to expire at the end of 2025.

- Employee Cost Shock: If these subsidies are not extended by Congress, employees who purchase coverage through the individual exchange could face a sharp spike in their personal healthcare costs. A KFF analysis suggests that subsidized enrollees could see their premium payments more than double on average in 2026.

- Talent Retention Risk: While this directly impacts employees, it creates a serious concern for small businesses. A massive increase in employee healthcare costs could lead emplopyers to degrading their benefits package in order to cut back on costs. Actions like this make it harder to attract and retain top talent, especially when competing with larger companies that offer more stable and robust benefits packages.

Preparing for Open Enrollment

The message is clear, healthcare costs are continuing to rise and it is only compounding year over year. You can’t just keep taking on these cost increase ever year. Some ways small business owners and HR professionals can proactively manage the coming financial challenges are by

1. Re-evaluating Your Benefits Strategy

- Explore Plan Design Changes: Learn about high-deductible health plans (HDHPs) paired with Health Savings Accounts (HSAs). While this shifts some costs, the lower premiums and tax-advantaged savings can be a compelling and affordable option for employees.

- Consider Alternative Funding: For companies with 50 or fewer full-time employees there are options like Health Reimbursement Arrangement (HRAs) and Individual Coverage Health Reimbursement Arrangements (ICHRAs) that provide small group plans to drastically lower plan costs..

- Assess Buy-Up Options: Provide a tiered plan lineup with “good, better, best” options. This allows employees who want richer coverage to pay more, while enabling your company to manage its baseline costs more effectively.

2. Exploring All Plan Options

- Don’t Settle for the Renewal: The quote from your current carrier is just a starting point. Use a benefits broker to shop and compare plans across multiple insurance companies, ensuring you find the best balance of affordability and coverage.

- Leverage Broker Expertise: A skilled broker can navigate the complex market on your behalf and help you find creative solutions to mitigate rising costs.

3. Educating and Empowering Your Team

- Communicate Transparently: Be honest with your employees about the state of healthcare costs. Provide them with resources and educational materials to help them understand their plan choices and the implications of the expiring federal subsidies.

- Promote Wellness Programs: Invest in employee wellness programs and telehealth options. A healthier workforce can lead to lower claims costs and increased productivity – benefiting everyone involved.

It is essential to take a look at your company benefits plan and learn about creative ways to save money. There are other options beyond simply accepting premium hikes degrading the benefits you already offer. There are ways to protect both your company’s bottom line and your most valuable asset: your employees. The time to prepare is now, before renewal season arrives and puts your budget at risk and your team under stress!

Sources

Stay in the know!

We share insightful insurance news and resources with you. We never share or sell your personal information.

More Insurance News & Articles

Planning Strategy: Using Life Insurance To Pay Off Debt

Life comes with its fair share of expenses—whether it’s a mortgage on your home, a car loan, or even credit card bills. These debts are usually manageable when you’re around to help pay them off.

Coverage for funeral costs, burial expenses, and other end-of-life costs

While it’s not something most of us like to think about, planning for final expenses is a way to protect your family from financial stress during an already emotional time.

Tax Benefits: The tax advantages of life insurance

When you're shopping for life insurance, you’re likely thinking about [...]

How life insurance provides financial protection for your loved ones

When we talk about life insurance, we're really talking about [...]